4 charts reveal G7 countries need enhanced corporate climate action

Jun 9th 2021

By Lila Karbassi, Chief of Programmes, UN Global Compact and Chair of SBTi Board and Alberto Carillo Pineda, Director of science-based targets at CDP and a Steering Committee Member at the SBTi

As the COVID-19 pandemic shook the global economy, many realized “business as usual” wasn’t going to cut it anymore. Despite the ongoing challenges, the past months have seen record numbers in corporate climate commitments and in April the Race to Zero announced their campaign has over 3,000 businesses, investors, cities and regions committed to net-zero. In addition, all of the G7 countries have long-term net-zero commitments. Businesses and governments alike are seeing opportunities in the zero-carbon economy and corporate greenhouse gas (GHG) emissions reductions targets have gone mainstream.

Yet, new research from the SBTi, led by CDP and the UN Global Compact, reveals that major G7 indexes are far from being aligned with the Paris Agreement goals when looking at corporate ambition in the shorter term (2025 - 2035). Of all leading G7 indexes, none are aligned with a 2°C pathway, much less with the 1.5°C trajectory that is so urgently needed to avoid the worst impacts of climate change. Instead, they are - on average - on a dangerous 2.95°C pathway. The G7 economies cover nearly 40% of the global economy and approximately 25% of global GHG emissions, so the businesses making up the G7 have a responsibility to lower their emissions.

The key indexes assessed in this report comprise the stocks of the largest companies listed on the main stock exchanges of G7 countries. Therefore, the temperature rating of these indexes is a reflection of the climate ambition amongst the largest listed companies in these countries, weighted by the relative size of the emissions of each of the companies in the index. If leading country indexes are unaligned with climate goals, so too will all the capital invested passively in them.

How do Leading G7 Country Indexes Measure Up?

So how do the indexes in the G7 countries match up? There are several findings from the indexes and the capital that flows through them. These four charts show how far countries are from reaching 1.5°C, as well as the reasons why, and where we can do better.

An overall look: Germany’s DAX 30 index has the best temperature rating, while the UK FTSE 100 and Canada’s SPTSX 60 indexes have the worst.

Figure 1: Index Temperature Scorecard as of 30 April 2021

What are the trajectories of companies? It’s split, but measuring below 3°C is not enough and too many companies are still in this category. In France’s CAC 40 and Germany’s DAX 30, 50% or more score below 3.2°C, while in Italy’s FTSE MIB and Canada’s SPTSX 60, over 70% are above 3.2°C.

Figure 2: G7 Index Companies Temperature Scopes (Scopes 1+2)

Where’s the biggest gap? Scope 3 emissions. When we consider the indirect emissions attributable to a company for the materials that they procure, services that they contract and products that they sell, the temperature rating for companies scores worse. For example, the number of companies in France’s CAC 40 that meet 1.5°C or well below 2°C drops 10% when including scope 3 emissions.

Figure 3: G7 Index Companies Temperature Scopes (Scopes 1+2+3) as of 30 April 2021

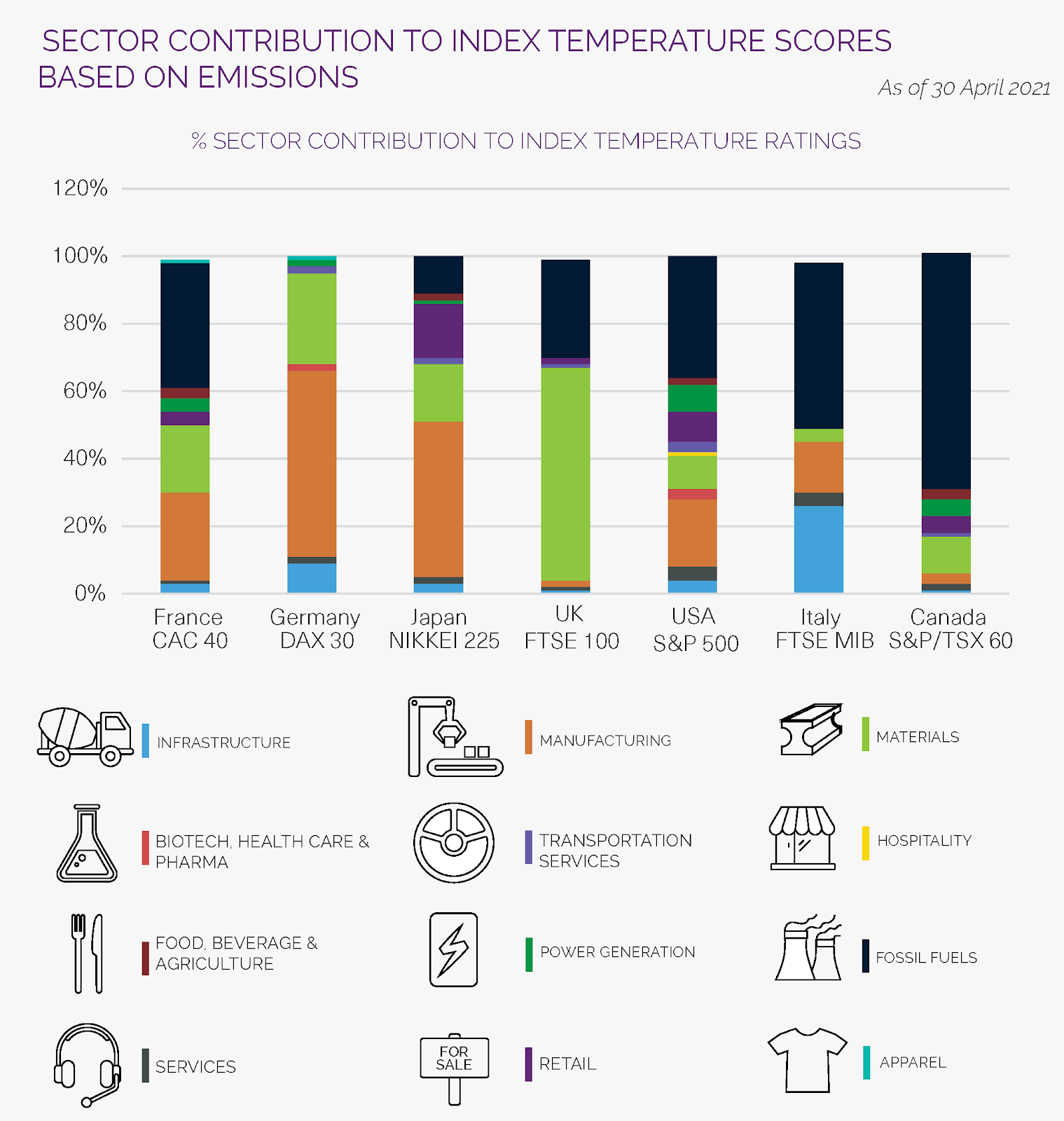

These seven leading indexes are also facing a barrier to reaching 1.5°C pathways: fossil-fuel dependency. In the G7 countries, a small number of high emitting companies in the fossil fuel and manufacturing industries are dominating the share of emissions. The investment in new fossil fuel supply past 2021 is incompatible with reaching 1.5°C, underscoring the importance of shifting to renewable energy. These high-emitting companies are keeping indexes from being more closely aligned to 1.5°C, as the SBTi finds that 35 of the FTSE 100 companies have already committed to align with the most ambitious pathway but this progress is overshadowed by a lack of action in these industries.

Figure 4: Sectoral Contribution to Index Temperature Scores based on Emissions as of 30 April 2021

How Can Companies Help Achieve a Paris-Aligned Global Economy?

These findings show that, aside from the momentum we’ve seen over the past few years, there is still a long journey ahead. The growing trend towards long-term target setting and net-zero pledges is compelling, but not moving the needle yet. The majority of targets still need the credibility and grounding in science to meet Paris goals. Short term action paired with long term plans aligned with climate science is how we can get there. We need to halve greenhouse gas emissions by 2030 and hit net-zero emissions by 2050.

Over 70% of emissions generated by companies in the German DAX 30 are currently covered by science-based targets. This is the highest percentage when compared to other indexes, explaining how DAX scores the best temperature rating of 2.2°C.

Businesses no longer have to choose profit or planet; they can go hand in hand. If public and private sector actors can align their ambitions and use science-based targets to set short- and long-term goals, countries will unlock a profitable and sustainable future. There are areas that need ambitious action now to achieve this mission: financial institutions, value-chain engagement, scaling up access to capital for SBTs and encouraging the Ambition Loop between government and corporate players, a positive feedback cycle in which private sector action and government policies reinforce one another. Although recent actions by the G7 ministers and the U.S. government showcase ambition, more clarity is needed from governments.

If policymakers leverage their regulatory power and incentivize the adoption of science-based targets across all industries and countries, their stock indexes and the capital flowing through them can get in line with the 1.5°C goal of the Paris Agreement.

See the full report here.